Japan presents a fascinating paradox for international travelers. Despite being one of the world’s most technologically advanced nations, it remains surprisingly cash-centric in many aspects of daily commerce.

If you’re planning a trip and wondering “Can I use my debit card in Japan?” the answer is yes—but with important caveats.

Understanding Debit Card Acceptance in Japan

The Cash Culture of Japan

Japan has a deeply ingrained cash culture that persists even as other developed economies increasingly go cashless. This preference for physical currency stems from several factors:

- Cultural values around the tangibility and security of physical money

- A societal emphasis on privacy in financial transactions

- Historically low crime rates making cash carrying relatively safe

- A general aversion to debt and credit-based spending

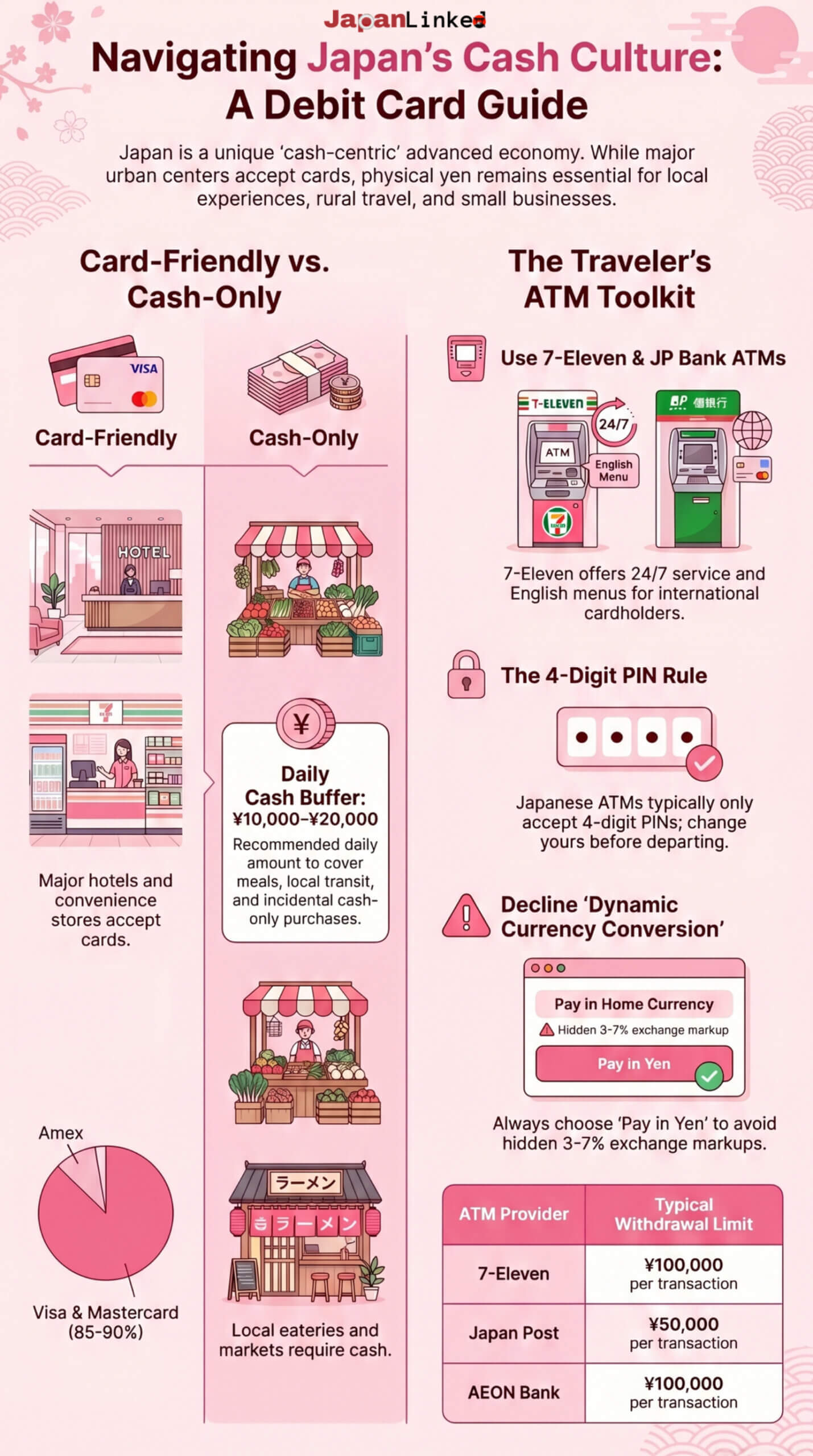

Many Japanese citizens carry significant amounts of cash for daily expenses, and it’s not uncommon to see people making large purchases with physical currency. This cultural context is important to understand as you prepare for your visit.

Where Debit Cards Are Commonly Accepted

Your debit card will generally be welcomed at:

- Major hotels and ryokans (traditional Japanese inns) in tourist areas

- Department stores and shopping malls in urban centers

- Chain restaurants and larger eateries in cities

- Tourist attractions and popular destinations

- Train stations for purchasing tickets (particularly in Tokyo, Osaka, and Kyoto)

- Convenience store chains like 7-Eleven, Lawson, and Family Mart

- High-end restaurants and international establishments

Many of these locations have adapted to accommodate the growing number of international visitors, especially following Japan’s tourism boom in recent years.

Where Cards Are Rarely Accepted

Be prepared to use cash at:

- Traditional markets and street food stalls

- Small, family-run restaurants and local eateries

- Vending machines (though this is gradually changing)

- Taxi services outside major urban areas

- Rural attractions and accommodations

- Local shops and businesses outside tourist zones

- Traditional ryokans in less-visited regions

A common experience for travelers: discovering a charming local restaurant only to find they don’t accept cards at all. Always have yen on hand for these authentic experiences!

The Importance of Cash Backup

Even with a debit card, carrying Japanese yen is essential for several reasons:

- Emergency situations where card networks might be temporarily down

- Small purchases where merchants might have minimum card transaction amounts

- Access to local experiences that operate on cash-only basis

- Transportation in areas where IC cards or credit cards aren’t accepted

- Peace of mind knowing you’re prepared for any payment scenario

A good rule of thumb is to carry enough cash to cover a full day’s expenses, including meals, local transportation, and incidental purchases. ¥10,000-¥20,000 (approximately $70-$140) is typically sufficient for daily needs, though this varies based on your travel style and itinerary.

Remember that Japan is generally very safe, with low rates of theft and pickpocketing, making carrying cash less risky than in many other destinations. Still, normal travel precautions apply—use hotel safes when available and be discreet when handling large amounts of money.

Finding ATMs That Accept Foreign Debit Cards

Japan’s reputation for being a cash-based society extends to its ATM infrastructure, which can initially seem challenging for international visitors. However, several reliable ATM networks throughout the country specifically cater to foreign cards.

7-Eleven ATMs: The Traveler’s Best Friend

7-Eleven convenience store ATMs are widely considered the gold standard for foreign card users in Japan. With over 25,000 locations nationwide, these ATMs offer:

- 24/7 availability in most locations

- English language interface

- Compatibility with major international cards

- Lower fees compared to some other options

- Reliable service even during Japanese holidays

These ATMs are so dependable that many experienced travelers to Japan recommend planning accommodations near a 7-Eleven for peace of mind.

Japan Post Bank (JP Bank) ATMs

Japan Post Bank ATMs are another excellent option found at post offices throughout the country. While their operating hours are more limited than 7-Eleven (typically 9:00 AM to 7:00 PM on weekdays, shorter hours on weekends), they offer:

- Widespread availability, even in rural areas

- English language support

- Acceptance of major international cards

- Relatively low withdrawal fees

Note: Many JP Bank ATMs stop international card service earlier than their posted closing times, often around 5:00 PM.

Other Reliable ATM Networks

Several other ATM networks accept foreign cards with varying degrees of accessibility:

| ATM Network | Hours | Foreign Card Compatibility | English Available | Notes |

|---|---|---|---|---|

| Family Mart | 24/7 in most locations | Very good | Yes | Growing network with increasing reliability |

| Lawson | 24/7 in most locations | Good | Yes | Available in most Lawson stores |

| AEON Bank | Mall hours (typically 9:00 AM-9:00 PM) | Very good | Yes | Found in AEON shopping malls |

| Citibank | Varies by location | Excellent | Yes | Limited locations but very foreigner-friendly |

International Network Compatibility

The compatibility of your debit card depends primarily on which payment network it belongs to. Here’s a quick reference guide:

- Visa/Plus: Highest acceptance rate at Japanese ATMs

- Mastercard/Cirrus/Maestro: Very good acceptance at major ATM networks

- UnionPay: Increasingly accepted, especially in tourist areas

- American Express: Limited acceptance, primarily at 7-Eleven ATMs

- Discover/Diners Club: Most limited acceptance, check with your card issuer before traveling

Finding ATMs with English Options

Almost all ATMs that accept foreign cards offer an English language option, typically accessible via a button on the initial screen. The interface is usually straightforward, with clear instructions for international users.

ATM Withdrawal Limits and Timing

Be aware of these important considerations when planning ATM withdrawals:

- Daily limits: Japanese ATMs typically allow ¥50,000-¥100,000 per transaction, with a maximum of ¥200,000-¥300,000 per day

- Your bank’s limits: Your home bank may impose lower daily withdrawal limits

- Transaction timing: Some ATMs don’t process international transactions during late-night hours (even if they’re physically accessible)

- Holiday availability: During Japanese holidays, some ATMs (except 7-Eleven) may not process international transactions

ATM Locator Tools

Before your trip, bookmark these useful resources:

- The Seven Bank ATM locator for finding 7-Eleven ATMs

- The Japan Post Bank ATM locator for post office ATMs

- Your card issuer’s global ATM locator tool

Many travelers find it helpful to download offline maps with ATM locations marked before arriving in Japan, especially if you’re unsure about mobile data access during your trip.

Understanding Fees and Charges When Using Debit Cards in Japan

When using your debit card in Japan, understanding the potential fees is crucial to avoid unwelcome surprises on your bank statement. Japanese ATMs and your home bank may both charge various fees that can quickly add up during your trip.

Foreign Transaction Fees From Your Bank

Most banks charge foreign transaction fees when you use your debit card abroad. These typically range from 1% to 3% of each transaction amount. For example, if you withdraw ¥10,000 (approximately $70), you might pay an additional $0.70 to $2.10 in fees.

Pro Tip: Some banks offer travel-friendly debit cards with zero foreign transaction fees. Check if your bank offers such cards or consider opening an account with one that does before your trip.

Banks that commonly offer no foreign transaction fee debit cards include Charles Schwab, Capital One 360, and some digital banks like Wise or Revolut.

ATM Operator Fees in Japan

In addition to your bank’s fees, Japanese ATM operators often charge their own fees:

- 7-Eleven ATMs: ¥110-¥220 per withdrawal

- Japan Post Bank (JP Bank): ¥110-¥220 per withdrawal

- Other bank ATMs: Fees can range from ¥110 to ¥440 depending on the bank and time of day

These fees are typically higher during “off-hours” (evenings, weekends, and holidays) and lower during standard banking hours.

Dynamic Currency Conversion Pitfalls

When making purchases or withdrawing money, you may be offered the option to pay in your home currency rather than Japanese yen. This service is called Dynamic Currency Conversion (DCC), and it’s almost always a bad deal for travelers.

DCC typically includes:

- A hidden markup of 3-7% on the exchange rate

- Additional service fees in some cases

- Less favorable rates than what your card network would provide

Always choose to pay in the local currency (Japanese yen) when given the option. This allows your card’s network (Visa, Mastercard, etc.) to handle the conversion, which is almost always more favorable.

Daily Withdrawal Limits

Be aware of two types of limits that may restrict your cash access:

- Your bank’s daily ATM withdrawal limit: Typically $300-$1,000 per day

- Japanese ATM withdrawal limits: Often around ¥50,000-¥100,000 (approximately $350-$700) per transaction

| ATM Provider | Typical Withdrawal Limit |

|---|---|

| 7-Eleven | ¥100,000 per transaction |

| Japan Post | ¥50,000 per transaction |

| AEON Bank | ¥100,000 per transaction |

If you need to access more cash, you may need to make multiple withdrawals at different ATMs or on consecutive days. Consider contacting your bank before traveling to temporarily increase your daily withdrawal limit.

Exchange Rate Considerations

The exchange rate you receive when using your debit card abroad is determined by:

- Card network rate: Visa, Mastercard, and other networks set their own exchange rates, which are typically very close to the mid-market rate

- Bank markup: Some banks add their own markup to the network rate

- Time of transaction: Exchange rates fluctuate throughout the day

To get the best exchange rates:

- Monitor exchange rate trends before your trip using apps like XE Currency or Wise

- Avoid airport currency exchange kiosks which typically offer poor rates

- Make larger, less frequent withdrawals to minimize per-transaction fees

- Consider locking in rates with a multi-currency account if the yen is particularly favorable before your trip

Understanding these fee structures and planning accordingly can save you significant money during your Japanese adventure, allowing you to spend more on experiences and less on banking fees.

How to Prepare Your Debit Card Before Traveling to Japan

Preparing your debit card before your trip to Japan can save you from unnecessary stress and financial headaches. Follow these essential steps to ensure smooth transactions throughout your journey:

Notify Your Bank of Travel Plans

Always inform your bank about your travel dates and destination before departing for Japan. This simple step prevents your card from being flagged for suspicious activity when foreign transactions suddenly appear. Many banks offer multiple ways to set up travel notices:

- Through your online banking portal

- Via your bank’s mobile app

- By calling customer service directly

- In person at your local branch

Most banks allow you to set travel notices 1-90 days before your departure. Without this notification, you might find yourself stranded with a blocked card due to suspected fraud.

Confirm International Activation

Not all debit cards are automatically enabled for international use. Contact your bank specifically to verify that your card is activated for transactions in Japan. Some banks require explicit authorization for overseas transactions as a security measure.

When speaking with your bank representative, ask:

- “Is my card already enabled for international transactions?”

- “Are there any restrictions on using my card in Japan?”

- “Do I need to activate any special features for overseas use?”

Set Up a Travel Notice

A travel notice (sometimes called a “travel alert”) is a specific notification to your bank about your international travel plans. This differs slightly from a general notification as it typically includes:

- Your exact travel dates

- Countries you’ll be visiting (Japan and any layover countries)

- Contact information while abroad

Setting up a proper travel notice can typically be done:

- Online through your bank’s secure portal

- Through your banking app under “card settings” or “travel plans”

- By phone with customer service

Pro tip: Set your travel dates a few days longer than planned to account for any unexpected delays or trip extensions.

Ensure 4-Digit PIN Compatibility

Japanese ATMs typically only accept 4-digit PINs. If your debit card has a PIN longer than 4 digits, contact your bank to change it before your trip. This is a crucial step that many travelers overlook.

Additionally, make sure you know your PIN by heart—Japan is not the place to realize you’ve forgotten it, as PIN retrieval from abroad can be complicated.

Check Daily Withdrawal Limits

Understanding your card’s daily withdrawal limits is essential for budgeting your trip:

- Bank-imposed limits: Your home bank likely has daily ATM withdrawal limits (typically $300-$1,000 or equivalent)

- Japanese ATM limits: Japanese ATMs often have their own withdrawal limits (usually around ¥50,000-¥100,000 per transaction)

- Foreign withdrawal limits: Some banks impose special limits for international withdrawals that differ from domestic ones

If your standard limit seems too low for your travel needs, request a temporary limit increase from your bank before departure. This can usually be arranged for the specific duration of your trip.

Bring Backup Payment Methods

Never rely solely on your debit card in Japan. Smart travelers prepare multiple payment options:

| Backup Method | Benefits | Considerations |

|---|---|---|

| Secondary debit card | Access to another account if primary card is lost/stolen | Keep in separate location from primary card |

| Credit card | Better fraud protection; emergency funds | Higher fees for cash advances |

| Cash (USD/EUR) | Can be exchanged at airports/hotels | Less favorable exchange rates than ATM withdrawals |

| Prepaid travel card | Locked-in exchange rates; no bank account access | May have activation/reload fees |

| Digital payment apps | Convenient for certain locations | Limited acceptance in Japan |

Store these payment methods separately from each other. Keep one card in your hotel safe, another in your wallet, and perhaps emergency cash in a hidden money belt. This strategy ensures you’re never completely without funds if theft or loss occurs.

Taking these preparatory steps before your Japanese adventure will significantly reduce the likelihood of financial disruptions and allow you to focus on enjoying your trip rather than solving banking emergencies from abroad.

Step-by-Step Guide to Using ATMs in Japan

Navigating Japanese ATMs can be intimidating for first-time visitors, especially with interfaces that may initially appear in Japanese. Follow this detailed guide to ensure a smooth ATM experience during your travels.

1. Locate a Compatible ATM

First, find an ATM that accepts foreign cards. Your best options include:

- 7-Eleven ATMs (available 24/7)

- Japan Post Bank (usually available 8:45 AM to 7:00 PM)

- Family Mart and Lawson convenience store ATMs

- AEON Bank ATMs in shopping malls

Pro tip: The 7-Eleven ATMs are widely considered the most reliable for foreign cards and are available around the clock.

2. Select English Language Option

Upon approaching the ATM:

- Look for the “English” button, typically located in the corner of the screen

- Touch this button before inserting your card

- The interface will immediately switch to English instructions

![ATM language selection button illustration]

3. Insert Your Card Correctly

Pay attention to the card orientation:

- Most Japanese ATMs require you to insert your card with the chip facing up

- Look for the card icon on the machine showing the correct orientation

- Insert the card firmly but gently until you feel it engage

4. Select “Withdrawal” Option

After the card is recognized:

- Choose “Withdrawal” or “Cash Withdrawal” from the menu options

- Some ATMs may ask you to select your account type (checking/savings)

- Select the appropriate account linked to your debit card

5. Enter Your PIN Correctly

Security is paramount:

- Enter your 4-digit PIN when prompted

- Cover the keypad with your other hand for privacy

- Note that Japanese ATMs only accept 4-digit PINs – cards with longer PINs may not work

6. Choose Amount Within Limits

Be aware of withdrawal limits:

- Most ATMs have a maximum withdrawal limit of ¥50,000-¥100,000 per transaction

- Daily limits vary by bank and ATM operator

- Your home bank may impose its own daily withdrawal limit

- Select an amount in increments offered (typically ¥10,000)

7. Decline Dynamic Currency Conversion

This is crucial to avoid excessive fees:

- If prompted to withdraw in your home currency or Japanese yen, always select Japanese yen

- Choosing your home currency activates Dynamic Currency Conversion (DCC), which typically includes unfavorable exchange rates and additional fees

- The screen may make the home currency option look more appealing, but resist this temptation

8. Confirm Transaction Details

Before finalizing:

- Review the withdrawal amount

- Check any fees displayed (typically ¥110-¥220 per transaction)

- Confirm by pressing the appropriate button (usually green)

9. Collect Your Card and Cash

Don’t walk away too soon:

- Japanese ATMs typically return your card first, then the cash

- Wait for both to be dispensed before leaving

- Listen for the beeping sound that indicates your card is being returned

- Take your receipt if offered (useful for tracking expenses)

10. Count Your Money Discreetly

For safety and cultural reasons:

- Step aside from the ATM

- Count your money discreetly – counting cash openly is considered inappropriate in Japan

- Store your money securely before walking away

Common ATM Error Messages

If you encounter problems, these are common error messages and solutions:

| Error Message | Likely Cause | Solution |

|---|---|---|

| “This card cannot be used” | Card incompatibility | Try another ATM network |

| “Insufficient funds” | Reaching daily limit or account balance issue | Check your balance or try a smaller amount |

| “Invalid PIN” | Incorrect PIN entry | Carefully re-enter your PIN |

| “Transaction canceled” | Time limit exceeded | Start the process again |

Remember that ATM availability and operating hours can vary, especially outside major cities. Plan your cash needs accordingly, and always have a backup payment method available.

Comparing Major Debit Card Networks in Japan

When planning your trip to Japan, understanding which debit card networks are widely accepted can save you significant hassle.

Not all card networks are created equal in the Japanese market, and knowing the differences can help you decide which cards to bring.

Visa vs. Mastercard Acceptance Rates

Visa and Mastercard are the most widely accepted international card networks in Japan, but there are subtle differences between them:

- Visa enjoys slightly higher acceptance rates, particularly at smaller merchants and in rural areas. Approximately 90% of card-accepting establishments will take Visa.

- Mastercard follows closely with about 85-88% acceptance at card-compatible locations.

Both networks are universally accepted at major department stores, hotel chains, and tourist destinations in cities like Tokyo, Osaka, and Kyoto.

American Express Limitations

If you rely on an American Express-linked debit card, be prepared for more limited acceptance:

- Only about 40-50% of card-accepting merchants in Japan take American Express

- Primarily accepted at high-end hotels, luxury retailers, and international restaurant chains

- Rarely accepted at smaller establishments, local restaurants, and shops outside major tourist areas

- ATM compatibility is significantly more restricted compared to Visa and Mastercard

American Express cardholders should always carry alternative payment methods when traveling throughout Japan.

Regional Differences in Acceptance

Card acceptance varies significantly across different regions of Japan:

| Region | Card Acceptance Level | Notes |

|---|---|---|

| Tokyo/Osaka | High (80-90%) | Most establishments accept major cards |

| Kyoto | Moderate-High (70-85%) | Traditional establishments may be cash-only |

| Hokkaido/Okinawa | Moderate (60-75%) | Tourist areas have good acceptance |

| Rural Japan | Low (30-50%) | Cash is strongly preferred |

Urban centers and tourist destinations generally offer better card acceptance than rural and traditional areas.

Chip-and-PIN vs. Magnetic Stripe Performance

The technology in your card makes a significant difference in Japan:

- Chip-and-PIN cards perform best, with near-universal compatibility at modern terminals

- Magnetic stripe cards face increasing rejection rates as Japan transitions to more secure systems

- Many Japanese payment terminals now require PIN entry rather than signatures

- Some unmanned payment kiosks (like ticket machines) will only accept chip cards

“Always ensure your card has chip technology before traveling to Japan. Magnetic stripe-only cards are becoming increasingly difficult to use.”

Contactless Payment Options

Contactless payment adoption is accelerating in Japan, particularly since the pandemic:

- Visa payWave and Mastercard PayPass contactless functionality works at an increasing number of locations

- Major convenience store chains (7-Eleven, Lawson, FamilyMart) now accept contactless payments

- Transit systems in Tokyo and other major cities accept contactless international cards

- Apple Pay and Google Pay linked to your debit card work at terminals displaying their logos or the QUICPay or iD symbols

However, Japan’s own contactless payment systems like Suica, PASMO, and Edy generally cannot be linked to foreign debit cards directly.

The bottom line: Visa and Mastercard chip-enabled debit cards offer the best overall experience in Japan, while contactless functionality provides added convenience in urban areas. Always carry some cash as a backup, especially when venturing outside major cities.

Smart Strategies to Minimize Fees and Maximize Convenience

Using your debit card in Japan can be convenient, but without proper planning, fees can quickly add up. Here are proven strategies to keep your costs down while ensuring you always have access to your money.

Best Practices for ATM Withdrawals

To minimize fees and hassle when withdrawing cash in Japan:

- Make fewer, larger withdrawals rather than frequent small ones to reduce per-transaction fees

- Use 7-Eleven ATMs whenever possible as they’re the most reliable for foreign cards and typically charge lower fees

- Withdraw cash during business hours (9:00 AM to 7:00 PM), especially at Japan Post Bank ATMs which often have limited hours

- Avoid airport and tourist area ATMs which may charge premium fees

- Check your daily withdrawal limit before traveling and adjust if necessary

- Keep receipts from all ATM transactions to track fees and in case of disputes

When using ATMs, always select “without conversion” or “withdraw in local currency” when prompted to avoid dynamic currency conversion fees, which can add 3-7% to your transaction.

Using Debit Cards with No Foreign Transaction Fees

Not all debit cards are created equal when it comes to international travel:

| Card Type | Typical Foreign Transaction Fee | ATM Fee | Best For |

|---|---|---|---|

| Standard Bank Debit | 1-3% | $2-5 per withdrawal | Emergency use only |

| Travel-Friendly Debit | 0% | $0-2 per withdrawal | Regular use |

| Premium Bank Accounts | 0% | Often reimbursed | Frequent travelers |

Before your trip, consider:

- Opening a travel-focused checking account with banks that offer no foreign transaction fees

- Looking into online banks like Charles Schwab which reimburses all ATM fees worldwide

- Checking if your current bank has partner institutions in Japan that offer reduced fees

Optimal Withdrawal Amounts

Finding the sweet spot for ATM withdrawals can save you money:

“The ideal withdrawal amount balances minimizing per-transaction fees while not carrying excessive cash. For most travelers in Japan, ¥30,000-¥50,000 (approximately $200-$350) at a time is optimal.”

Consider:

- Calculating your daily budget and withdrawing 3-4 days’ worth of cash at once

- Factoring in your itinerary – withdraw more before heading to rural areas with fewer ATMs

- Being mindful of flat-rate fees – a ¥220 fee on a ¥10,000 withdrawal is effectively 2.2%, but only 0.44% on a ¥50,000 withdrawal

When to Use Credit vs. Debit

Strategically choosing between credit and debit cards can optimize your spending:

- Use debit cards for:

- Cash withdrawals at ATMs

- Purchases at smaller establishments that accept cards but charge extra for credit

- Daily expenses when you want to stick to a budget

- Use credit cards for:

- Large purchases like hotel stays and expensive meals

- Shopping at department stores and major retailers

- Situations where you need purchase protection

- Car rentals and other services requiring holds

Pro tip: Many credit cards offer better exchange rates and more robust fraud protection than debit cards, making them preferable for larger transactions when available.

Mobile Payment Alternatives

While Japan has been slow to adopt some international mobile payment systems, options are expanding:

- Apple Pay is increasingly accepted, especially in major cities and at chains like 7-Eleven, Lawson, and Family Mart

- Google Pay has more limited acceptance but works at some larger retailers

- Local mobile payment options like PayPay, LINE Pay, and Rakuten Pay are widespread but typically require a Japanese bank account or credit card

- Transportation IC cards like Suica and PASMO can now be added to Apple Wallet on compatible devices

For travelers with compatible devices, setting up Apple Pay or Google Pay with your travel-friendly cards before departure can provide an additional convenient payment method, especially in Tokyo and other major cities.

By implementing these strategies, you can enjoy the convenience of your debit card in Japan while keeping fees to a minimum and ensuring you always have access to your funds when needed.

Security Considerations When Using Debit Cards in Japan

Japan is generally considered one of the safest countries in the world, but financial security should never be taken for granted when traveling. Being aware of potential risks and taking proper precautions can help ensure your debit card experience remains trouble-free throughout your Japanese adventure.

ATM Skimming Awareness

While rare in Japan, ATM skimming—where criminals install devices to steal card information—can still occur, particularly in tourist-heavy areas:

- Inspect the card reader before inserting your card. Look for any loose, crooked, or additional pieces attached to the machine.

- Cover the keypad when entering your PIN, even if no one appears to be watching.

- Choose ATMs in well-lit, monitored locations such as inside convenience stores, bank branches, or shopping malls.

- Avoid standalone ATMs in isolated areas or those that appear unusually old or poorly maintained.

Many Japanese ATMs have built-in security features like privacy screens and shields, but remaining vigilant is still important.

PIN Protection Tips

Your PIN is the key to your account, making its protection essential:

- Never share your PIN with anyone, including travel companions.

- Use a unique PIN for your debit card that differs from other passwords.

- Memorize your PIN rather than writing it down in your wallet or phone.

- Position your body to block the keypad when entering your PIN.

- Be wary of “helpful” strangers offering assistance at ATMs—bank staff will never ask for your PIN.

What to Do If Your Card Is Lost or Stolen

Quick action is crucial if your debit card goes missing:

- Contact your bank immediately to report the loss and block the card.

- File a police report at the nearest koban (police box) or police station.

- Document the details of when and where you last used the card.

- Monitor your account for unauthorized transactions.

- Arrange for emergency funds through wire transfer services if needed.

Pro tip: Take a photo of your card (front and back) before traveling and store it securely in your email or encrypted cloud storage. This makes reporting much easier if your card is lost.

Emergency Contact Numbers for Major Banks

Save these international customer service numbers before traveling:

| Bank Type | Contact Information |

|---|---|

| U.S. Banks | Most have 24/7 collect call numbers on the back of cards |

| UK Banks | Typically offer +44 numbers for overseas assistance |

| EU Banks | Usually provide dedicated international support lines |

| Australian Banks | Generally maintain 24/7 overseas support numbers |

Important: Many banks have specific international emergency numbers different from their regular customer service lines. Verify and save the correct international support number for your specific bank before departure.

Using Secure ATM Locations

Not all ATM locations offer the same level of security. Prioritize these options:

- 7-Eleven ATMs are available 24/7, well-monitored, and consistently reliable for foreign cards.

- Post office ATMs are located in secure buildings with staff present during business hours.

- Major bank branches typically have security personnel and surveillance systems.

- Airport ATMs are monitored and often have staff nearby.

- Hotel ATMs in international hotels offer convenience and security.

Avoid using ATMs:

- In dimly lit areas

- On empty streets, especially late at night

- In establishments that appear questionable

- With unusual signage or handwritten instructions

By following these security practices, you can significantly reduce the risk of debit card fraud or theft while enjoying your time in Japan. Remember that preparation and awareness are your best defenses against potential financial disruptions during your travels.

Alternatives to Debit Cards in Japan

While debit cards can be useful in Japan, having backup payment methods is essential for a smooth travel experience. Japan’s cash-centric culture means you should always have alternative payment options ready.

Prepaid Travel Cards

Prepaid travel cards offer a convenient alternative to traditional debit cards with several advantages:

- Lower fees than many bank-issued debit cards

- Multiple currency support including Japanese yen

- No link to your main bank account, enhancing security

- Reloadable online or via mobile apps

Popular options include Wise (formerly TransferWise), Revolut, and N26, which typically offer competitive exchange rates and minimal fees. Load these cards before your trip and use them like regular debit cards at compatible merchants and ATMs.

Credit Card Options

Credit cards are more widely accepted in Japan than debit cards, particularly at:

- Hotels and ryokans

- Department stores

- Major restaurants

- Tourist attractions

- Transportation hubs

Visa and Mastercard have the highest acceptance rates, while American Express and Discover are less commonly accepted. Credit cards also offer additional travel benefits such as purchase protection, travel insurance, and often better exchange rates than many debit cards.

Cash Exchange Services

Given Japan’s cash-based economy, currency exchange services remain essential:

- Airport exchange counters (convenient but often with less favorable rates)

- Major banks in urban centers (better rates but limited operating hours)

- Specialized currency exchange shops in tourist areas like Shinjuku and Shibuya

- International ATM withdrawals to obtain yen directly

Pro tip: Compare rates before exchanging large amounts and consider splitting your exchanges between pre-trip and in-country services to hedge against rate fluctuations.

Mobile Payment Acceptance

While not as prevalent as in some other Asian countries, mobile payment options are growing in Japan:

| Payment Method | Acceptance Level | Best For |

|---|---|---|

| Apple Pay | Moderate | Major retailers, convenience stores |

| Google Pay | Limited | Chain stores, some restaurants |

| PayPay | Growing rapidly | Local businesses, taxis |

| LINE Pay | Popular with locals | Small merchants, online purchases |

| Alipay/WeChat Pay | Limited to tourist areas | Chinese-frequented establishments |

These services are increasingly available in urban centers and tourist destinations but remain less reliable in rural areas.

IC Cards: Suica and PASMO

Perhaps the most useful payment alternative for visitors are IC cards like Suica and PASMO:

- Primary function: Transit payment on trains, subways, and buses

- Secondary uses: Convenience stores, vending machines, some restaurants and shops

- Convenience factor: Tap-and-go technology, no signature or PIN required

- Availability: Purchased at train stations with minimal ID requirements

- Refundable: Remaining balance can be refunded (minus fee) when leaving Japan

These rechargeable cards can be topped up at train stations and convenience stores, making them ideal for daily transportation and small purchases. Many tourists find IC cards indispensable for navigating Japan’s extensive public transportation networks while also serving as a convenient payment method for everyday expenses.

“In Japan, having multiple payment options is not just convenient—it’s essential. An IC card for transit and small purchases, some cash for traditional establishments, and a credit card for larger expenses creates the ideal payment portfolio for travelers.”